By Darren Burns, Head of Investment Solutions at Glacier Invest

“Timing is everything”. There are many different variations of this quote, however, ultimately whether it is planned or by chance, the impact of timing can be the single difference between celebrating success or languishing in failure.

In the investment industry it is instilled in us that it is impossible to consistently and successfully time the market. History is proof of this as there have been many failed attempts to do so, and while there are a relatively small number of successful investors, they have also been wrong a large percentage of the time.

Timing risk

‘Timing risk’ is defined as “the speculation that an investor enters into when trying to buy or sell a stock based on future price predictions”[1]. While this is a major focus of asset managers – financial advisers and investors have much more unique tenure requirements.

Let’s not forget that the assumed lifespan of a collective investment scheme is infinite. With no end-point, it is managed very differently to individual portfolios. When a portfolio manager purchases a stock, he does so with the intention that there will be a positive return at some future date. This future date is undefined and mostly in direct contrast to the thinking required when managing individual client portfolios. Individual portfolios can have a number of predefined events, one of which is date of retirement. Some of these events can be so significant in the life of the investor that they may result in the need for a complete revaluation of the overall investment strategy.

Parts

1 and 2 of this article will provide more insight into two of the lesser known

risks that relate to timing. While these risks – and the impact they have on

investor portfolios – may be more unfamiliar, this in no way implies that they

are any less significant. In fact, ignoring these risks could result in the

difference between retiring successfully or not being able to retire at all.

Life-cycle risk

Last year, South Africa won the Rugby World Cup and the entire country celebrated. In fact, some are still celebrating! This was truly an exceptional achievement and came at a time when a generally dispirited nation needed inspiration. As I’m sure that the memory of this event remains front of mind for many South Africans, the same memory will linger as a sore point for English rugby supporters for years to come. Why is this relevant? The English rugby team actually gave us great example of how not to retire.

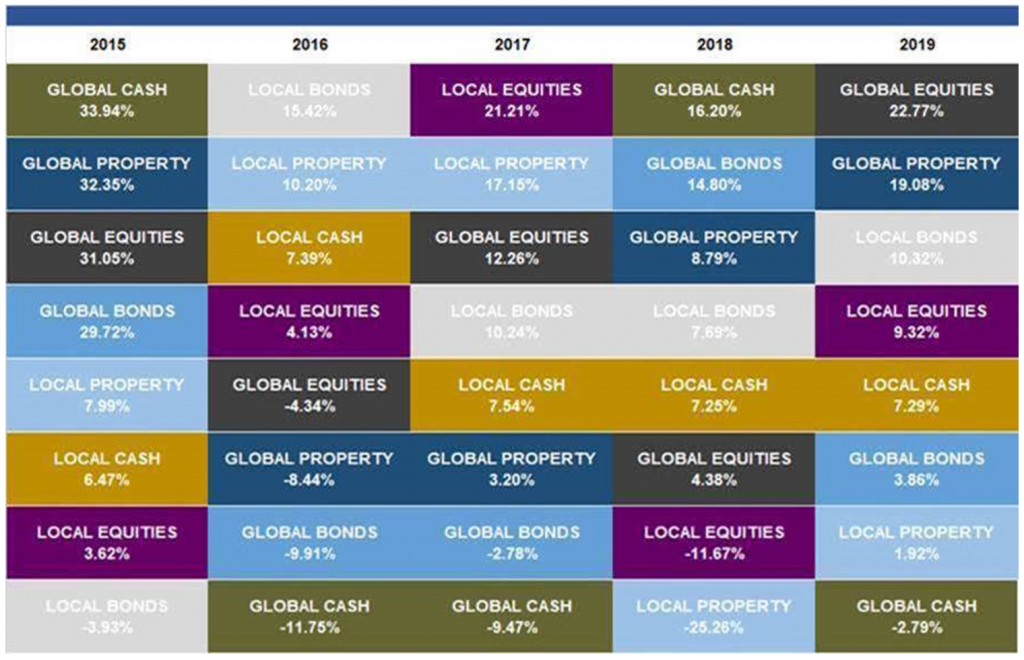

Overall the last five years have not been kind to the South African equity market. Apart from a positive turnaround in 2017, we have seen local stocks underperform SA bonds and cash in three of the last five years. See the table below.

Source: Glacier Research & Morningstar

In the case of the average pension/ owner, investing in Regulation 28 compliant, moderate risk funds would have mostly resulted in muted returns. This short-term underperformance is not a cause for concern for those with a long-term horizon, with some 20 years to retirement. For those who were or are near to retirement, however, these results may have a significant effect on how well they will retire and what type of lifestyle they can look forward to in their ‘golden’ years.

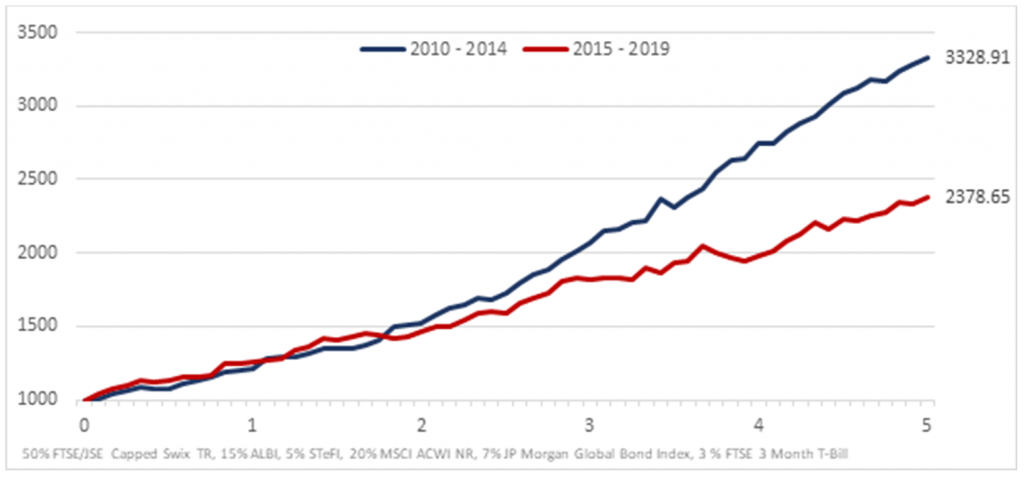

Let’s use a practical example to demonstrate this. The graph below shows the five-year returns of a balanced (Regulation 28 compliant Multi-Asset High Equity Index) portfolio between 2010-2014 and 2015-2019.

Source: Glacier Research & Morningstar

Assuming the investors have similar savings values (adjusted for inflation), the five-year returns prior to retirement resulted in significantly different amounts with which they would retire. In fact, someone who completed their salaried career in 2014 would have retired with almost 40% more wealth than someone who retired at the end of 2019. This is a very simplified example but external factors such as increased contributions, which usually occur later in life due to less debt (property paid off) and smaller fixed expenses (no more school fees), only exacerbates the problem.

So, how do we ensure that our retirement savings do not perform like England in the Rugby World Cup? England had a stellar performance throughout the majority of the tournament, only to collapse at the end when it counted the most. So the question we need to ask ourselves is: If we cannot successfully time the market over the short term, when it can have such a large impact on our retirement value, are we supposed to leave our future way of life at the mercy of where the market is in ‘the cycle’? The answer is no. While we cannot control market performances and while all risks can never be eliminated completely, there are ways and means to mitigate the life-cycle risk that we face. These will be explored further in Part 3 of this article.

“The question isn’t at what age I want to retire, it’s at what income” – George Foreman

[1] James Chen, Timing Risk, Investopedia, https://www.investopedia.com/terms/t/timingrisk.asp