By Mansoor Narker, Research & Investment Analyst at Glacier by Sanlam

After weeks of amassing armed forces and supplies around the border of Ukraine, Russian President Vladimir Putin has ordered his troops to move in and launch a full-scale invasion of its neighbour. Major western nations have responded by announcing sanctions, mainly targeted at Russia’s financial sector, politicians and wealthy oligarchs connected to Putin. While it is too soon to know exactly how the situation will play out, the impact has already been felt across global financial markets. With the global economy already fragile after the onslaught of the COVID-19 pandemic, supply chain disruptions and restarting of economies leading to a synchronised rise in inflation - the latest crises will certainly add fuel to the fire. Brent crude oil prices have spiked to over $100/barrel, reaching highs last seen in 2014, while liquified natural gas (LNG) prices have also risen to near record highs amid an already tight market. Although the Russian economy only contributes around 1.7% to global GDP, the country does have a larger influence in key commodities – which could have serious consequences for global growth and stability.

Impact on the commodity sector

Keenly aware of the damage it could bring to their own economies, major Western powers including the US, the UK and the European Union have not targeted sanctions against Russia’s commodity sector at this stage. In 2020, Russia was the world’s third-largest crude oil and petroleum supplier, pushing out 11% of global supply. The US, which itself has become the number one oil producer in the world - although it remains a net importer - receives about 7% of its crude supplies from Russia.

Although not a member of OPEC (Organisation of the Petroleum Exporting Countries), the cartel has placed an increased reliance on Moscow’s cooperation in recent years to coordinate the supply of oil and drive prices higher, resulting in Russia having increased its influence in this key commodity. Any major disruption of current supply could see crude spike as high as $150/barrel or more, a price at which economists from JP Morgan estimate could shave as much as three quarters off from global economic growth. The good news is such an increase would most likely be met with a strong supply response from major oil producing nations to counter any demand destruction. When it comes to LNG, Europe sources over 40% of its requirements from Russia (30% of that flows through Ukraine) with major European economies including Germany, France and Italy heavily reliant on Russian supply. While the continent has been sourcing more and more of its gas needs from the US, it would not be enough to plug any gaps if supplies from Russia were to be reduced.

Increased food inflation will place consumers under additional strain

The other key commodity at risk is wheat. Russia is the world’s largest supplier of wheat, and together with Ukraine – itself a major producer of wheat and corn – accounts for about 25% of global exports. With food prices already at their highest level in more than a decade, further disruptions of important agricultural inputs will only add to inflation fears and put consumers under additional stress. Another related risk is social upheaval that could be sparked should staples rise too much as a knock-on effect, particularly in more vulnerable nations in the Middle East and Africa, which receives more than 40% of its wheat and corn supplies from Ukraine.

Other important commodities emanating from Russia include nickel and its by-product, palladium, with the country being the largest producer of both metals, as well as titanium and urea used in fertilisers. Ukraine is also an important producer of neon, used in the manufacture of semiconductors, and accounts for 70% of global production.

Inflation pressures likely to persist

The key take-aways are that inflation pressures are likely to persist as a risk-premium would keep commodities elevated in the short term. This could also complicate matters for central banks, especially the European Central Bank (ECB), with the conflict potentially derailing growth in Europe at a time when they are grappling with multi-year high inflation. Officials from the ECB, some of whom were previously hawkish, have already stated that the withdrawal of stimulus measures may have to be delayed with the uncertain outlook. In the event of a prolonged conflict, the effects may ultimately be deflationary as trade and demand stalls. However, the series of increasingly harsher sanctions by Western allies including cutting off selected Russian banks from the SWIFT payments network and the effective freezing of the bulk of the Russian Central Bank’s $640 billion in foreign reserves indicate they intend to bring Russia to heel sooner than later by inflicting maximum damage to their economy. The Russian rouble has already lost as much as 29% of its value while the Russian Central Bank has hiked interest rates to 20% from 9.5% overnight and implemented capital controls in response.

Effect on South Africa and global markets

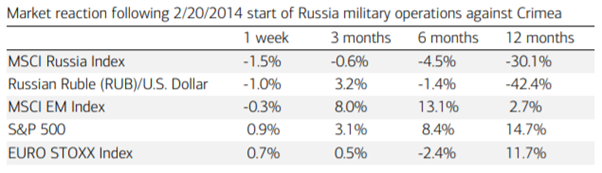

Closer to home, the tensions could also provide shorter-term tailwinds for the agricultural and mining sectors and provide further support for the fiscus but will place pressure on already pressured local consumers. Global markets, which initially suffered sharp losses on the day of the invasion, are holding up despite the volatility. In the case of a limited war, risk should find support as the risks are priced in and the worst-case outcome is avoided. Indeed, using history as a guide while acknowledging the key differences in the current environment, previous military operations in Ukraine by Russia in 2014 left little lasting impact on markets outside of the epicenter of the clashes. Of course, all bets are off should the event evolve into a much larger conflict.

Source: Merril, Bloomberg

Effect on investment portfolios

Investors concerned about their portfolios could use this opportunity, together with their financial adviser, to reassess and rebalance their exposures. While equities have over the long term shown to provide a superior source of risk-adjusted returns, a well-diversified portfolio across asset classes and within equities becomes more important as yields and volatility rise. Funds with higher resources and precious metals exposure stand to benefit in the current environment, and act as a rand hedge in the case of currency weakness, while consumer-facing stocks such as retailers and food producers may come under further pressure. Yields on SA government bonds have kept within range and offer compelling returns despite the risk-off sentiment. Developed markets as well as emerging markets will remain volatile until more certainty is attained with European markets more vulnerable to further weakness given their proximity to current events.