23 February 2023

ASISA (The Association for Savings & Investment South Africa) has certain suggested income drawdown levels for investors in living annuities, which are based on age and gender. These guidelines are advantageous, but they don’t necessarily include different risk scenarios. In this article, I present some easy-to-follow ideas which benefit the client and intermediary alike.

A simplified guideline

The following is a simplified guideline and investors should remember that the living annuity income level is not guaranteed, as the underlying investments are dependent on market conditions. The examples presented in this article attempt to find a good balance between income level, risk taken and income longevity.

The examples all use the following standard principles:

- The age of the client is used as a decimal figure. For example, age 55 becomes 5.5%, age 62 becomes 6.2% etc.

- I then deduct a factor of 1% to determine a suggested starting income level.

- The projections are then made with an annual income escalation of 5%.

- Inflation is selected at 5% (considered to be an accepted level for the long term, for as long as the SARB aims to keep the inflation band between 3% and 6%).

- I then compare the projections of a cautious portfolio (real plus 3% growth) with a moderate aggressive portfolio (real plus 5%) to note the different return profiles of a risk-adjusted portfolio.

These two risk profiles are selected as many clients want the typical balanced fund return profile but don’t want the volatility and sequence risk (the risk of a market drawdown just before, or just after, retirement). Many clients therefore prefer to select a cautious portfolio with its more acceptable volatility level, but which might not provide enough exposure to growth over the long term.

Thereafter, I also attempt to provide a possible solution to this risk-return dilemma.

The following graphs show these comparisons at ages, 55, 62, 68 and 73. I propose that these selected ages should be sufficient to make deductions that will cover most clients in a living annuity.

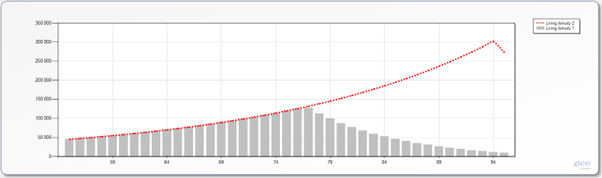

Age 55, income 4.5%

- The cautious portfolio will allow for an income growth until roughly age 77, after which the income will start to decline.

- In the moderate aggressive portfolio, however, the capital is sufficient to provide this same level of income until after the age of 90.

- This formula is therefore appropriate for younger clients, as long as they take on more risk.

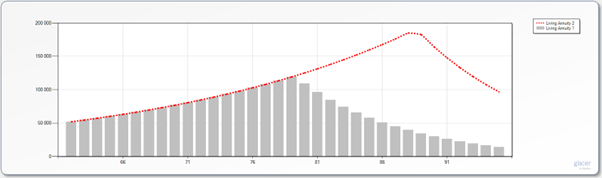

Age 62, income 5.2%

- The cautious portfolio again sustains the income need until roughly age 78, but thereafter the income starts to decline.

- The moderate aggressive portfolio is projected to supply an escalating income until roughly age 88, which suggests that a client at this age, who uses the age as decimal less 1% factor to determine the initial income, should have enough income.

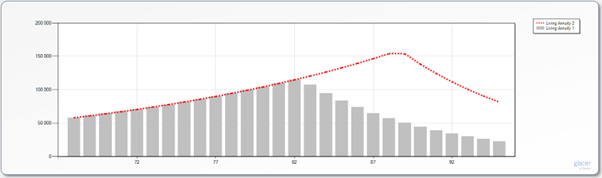

Age 68, income 5.8%

- The same pattern is evident, which again suggests that the higher risk portfolio should offer the better outcome over the longer term.

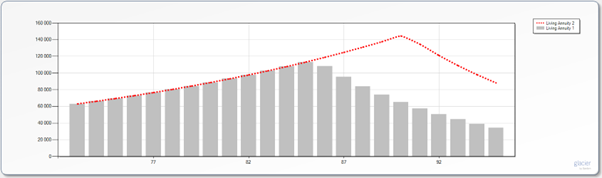

Age 73, income 6.3%

- The risk taken in a cautious portfolio seems to be sufficient for an older client, as the income is sustainable until roughly age 85. However, it again seems to be better if one can take on more risk as this extends the age at which the income starts to decline, to roughly 90.

Points for consideration

- Changing the age to a decimal, and then subtracting 1% to determine the starting income level, seems to be a relatively accurate way of ensuring an escalating income of 5% per annum, until roughly age 80.

- However, roughly 10% of the South African population do live beyond age 80, and where people have access to better medical care, this percentage is a lot higher.

- By taking on more risk, income longevity becomes less of a concern for the broader population as very few people do live up to the age of 90.

- For clients taking on a moderate aggressive risk, in line with most balanced funds, this is a suitable formula to determine the starting income.

- However, the volatility of a moderate aggressive portfolio not only makes the investment journey less comfortable for the client – due to the ups and downs of market movements – but also holds real risk over extended periods when markets are down, and this manifests in the sequence risk of the portfolio.

Therefore, if one uses this simplified formula to determine the initial income level, it is imperative to find a solution where a return of inflation plus 5% is possible, but at a volatility level similar to a cautious portfolio. This will allow for extra growth while protecting the client against sharp drawdowns, and, over time, sequence risk.

It is not possible to build a portfolio which offers these characteristics by using only normal collective investments, even if the portfolio is properly diversified. Once the portfolio has exposure to sufficient growth , the volatility and accompanying risks will follow. One therefore needs to consider alternative types of funds that have different return profiles, such as hedge funds (which can give a positive return during a crisis) as well as funds with underlying guarantees that smooth out the volatility. By combining funds such as these, clients have the opportunity to achieve a real return plus 5%, however, the volatility and sequence risk is lowered to that of a cautious portfolio.

What is the ideal solution?

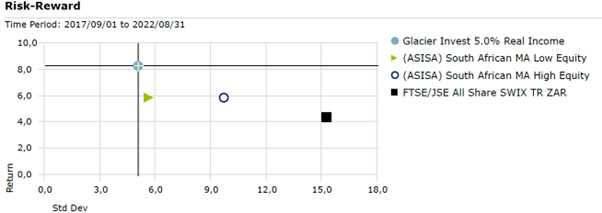

A portfolio that does this is the Glacier Invest 5% Real Income Solution. This portfolio uses hedge funds, smoothing portfolios (both local and offshore) as well as multi strategy alternatives which include, amongst others, private equity, and real .

Portfolios which guard against the downside risk tend to lag balanced funds during bull markets but manage to reduce downside and the sequence risk during adverse periods. The following table illustrates the return and risk profile of this portfolio when compared to the average cautious (low equity) and moderate aggressive (high equity funds) over the last five years (until end August 2022).

Not only did this portfolio outperform the average high equity fund over this period, but it also achieved this at a slightly lower risk than an average cautious fund (low equity).

Conclusion

- The formula where one uses the age of a client, changing it to a decimal and then subtracting 1% from it to determine the starting income of the client, does allow for an escalating income until roughly the age of 80, regardless the age of the client.

- However, if a client needs to reduce volatility and decides to rather opt for a cautious portfolio, income longevity remains an issue for those who live beyond age 80.

- By increasing the growth to a level of inflation plus 5%, via a moderate aggressive portfolio, one reduces the impact of longevity risk sharply, but the volatility and sequence risk will increase.

- By using the Glacier Invest 5% Real Income Solution, which incorporates alternative strategies and fund types, one can achieve the inflation plus 5% return, but at the volatility of a typical cautious portfolio.

- The formula to determine the initial income, as outlined above, can be achieved by using the Glacier Invest 5% Real Income Solution.