Anyone who has ever built a house knows that it’s quite a process. It invariably takes longer than anticipated and sometimes costs more than you expect. Retirement planning requires a similar approach – start with this expert guidance.

Glacier by Sanlam’s Through the Years research report conducted face-to-face interviews with 82 retirees to find out how they financially planned for retirement. Of those that retired comfortably, 82% had engaged with a financial adviser. Just as you don’t have to build your house alone, you don’t have to do retirement planning on your own – there are experts to help along the way.

The retirement worries to plan against

“In the same way that you create your dream home, you build your dream retirement,” says Patrick Sheehy, Head of Product Management at Glacier by Sanlam. “You need to plan, lay a solid fiscal foundation, and invest time and effort in the construction phase to ensure you create something that’s structurally sound. As with a house, you’re not in it alone. There are plenty of experts to guide you along the way.”

The research found that many retirees are concerned about the impact of inflation, supporting one’s family, minimal state support and the rising cost of living in South Africa. Most were worried about being a burden to their families and having insufficient funds to ‘last a lifetime.’ Dealing with death, divorce and illness had also thrown some retirees off-track with their savings.

To ensure you have a sufficient income to maintain your current lifestyle, while also covering you in the event of unexpected curveballs and providing you with some funds for fun, you need to plan in advance to construct a ‘house’ that lasts.

Here’s a guide to solid retirement planning

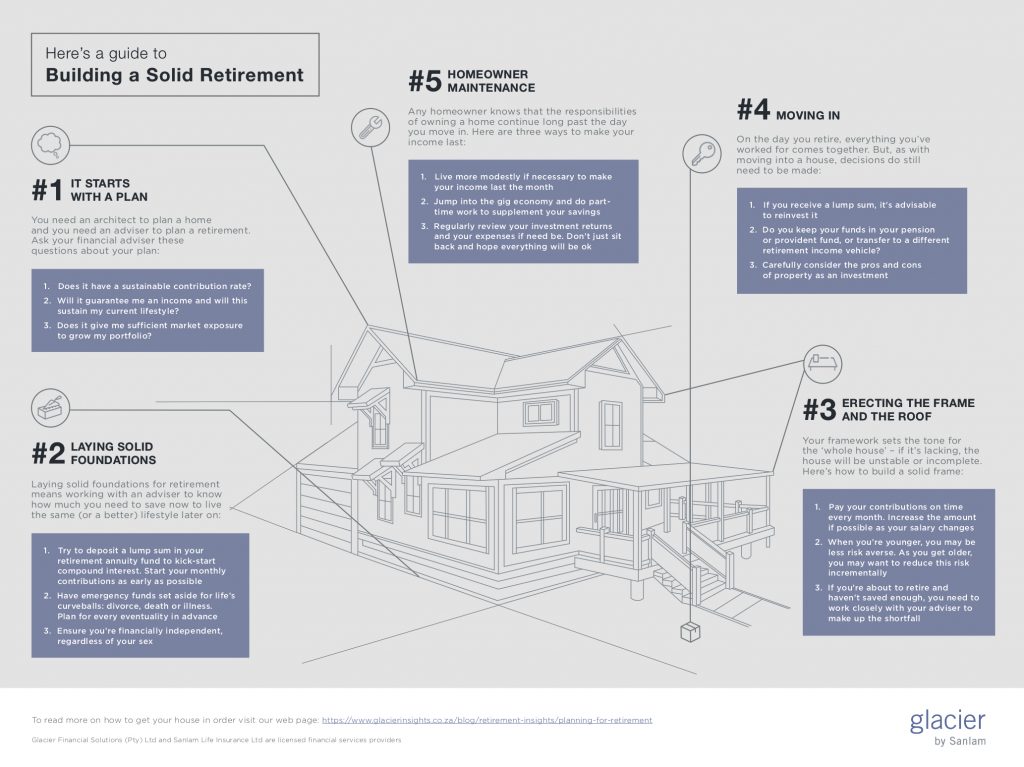

1. It starts with a plan

You build a house to stand the test of time. Likewise, you need to plan how best to invest your retirement savings to generate an income that lasts a lifetime. You’d never build a home without consulting an architect. In the same way, you probably shouldn’t plan your retirement without consulting an adviser. Ask your financial adviser these questions about your plan:

- Does it have a sustainable contribution rate?

- Will it guarantee me an income and will this sustain my current lifestyle?

- Does it give me sufficient to grow my portfolio?

- What are the costs and risks I take on?

- Will it adjust to my changing needs?

2. Lay solid foundations

Without solid foundations, any building is likely to collapse. Although you can sometimes amend ‘mistakes’, it’s tricky, time consuming and often more costly. As with most things in life – it’s wise to get it right the first time. Laying solid foundations for retirement means working with an adviser to know how much you need to save now to live the same (or a better) lifestyle later on. Remember, your income should grow with you – this is critical in retirement planning.

- Try to deposit a lump sum in your retirement annuity fund to kick-start . Start your monthly contributions as early as possible.

- Have emergency funds set aside for life’s curveballs. Some retirees said they were on track for retirement until divorce, death or illness happened. Plan for every eventuality in advance.

- Ensure you’re financially independent.

3. Erect the frame and roof

The frame is the heart of the building, so it’s critical it stays true to the plan and is constructed upon a strong foundation. From a retirement perspective, your framework sets the tone for the ‘whole house’ – if it’s lacking, the house will be unstable or incomplete. You also need to ensure you have a ‘roof’ over your head for your whole retirement – this means saving enough for a monthly income, and possibly supplementing this through part-time work post retiring.

- Pay your contributions on time every month. Try not to fall behind with these. Increase the amount if possible as your salary changes.

- Manage your risk (or get an adviser to manage it for you). When you’re younger, you may be less risk averse – a good time to take advantage of growth investment options. As you get older, you may want to reduce this risk incrementally.

If you’re close to finishing the house but you’re running out of funds (about to retire and haven’t saved enough), you need to work closely with your adviser to meet your goal. Some sacrifices may need to be made to ensure you make up the shortfall as part of a final push.

4. Moving in

Moving day is known for being stressful – but it’s incredibly rewarding as well. On the day you retire, everything you’ve worked for comes together. But, as with moving into a house, decisions do still need to be made:

- If you receive a lump sum, it’s advisable to reinvest it. Speak to your financial adviser.

- Do you keep your funds in your pension or , or transfer to a different retirement income vehicle?

- Carefully consider the pros and cons of property, if this is something you’re interested in investing in.

Think about how you’re going to spend your days. Draw up a plan with goals you want to achieve and bucket list travel destinations and activities you’re eager to tick off.

5. Maintain your hard work

Any homeowner knows that the responsibilities of owning a home continue long past moving in day. In fact, on-going maintenance is necessary to keep the building in top condition. In terms of retirement planning, this means:

- Living more modestly if necessary to make your income last the month.

- Jumping into the gig economy and doing part-time work to supplement your savings.

- Regularly review your investment returns and your expenses. Cut back, or cut out luxury expenses if need be. Don’t just sit back and hope everything will be okay.

Please consult with a financial adviser before you take any action regarding your savings and investments.